Value investing in Low income housing

Step I- Risk Elimination

Elimination of sub-optimal asset-classes– Investment in a real-estate fund is superior to direct investment in real estate due to higher diversification achieved through investment in multiple projects.

Elimination of risky segments– We noticed oversupply in segments such as retail/ malls and commercial/ office/ IT while other segments such as industrial/warehousing/ hotels etc. face political/ economic risk. Our research showed that residential projects would prove to be safest.

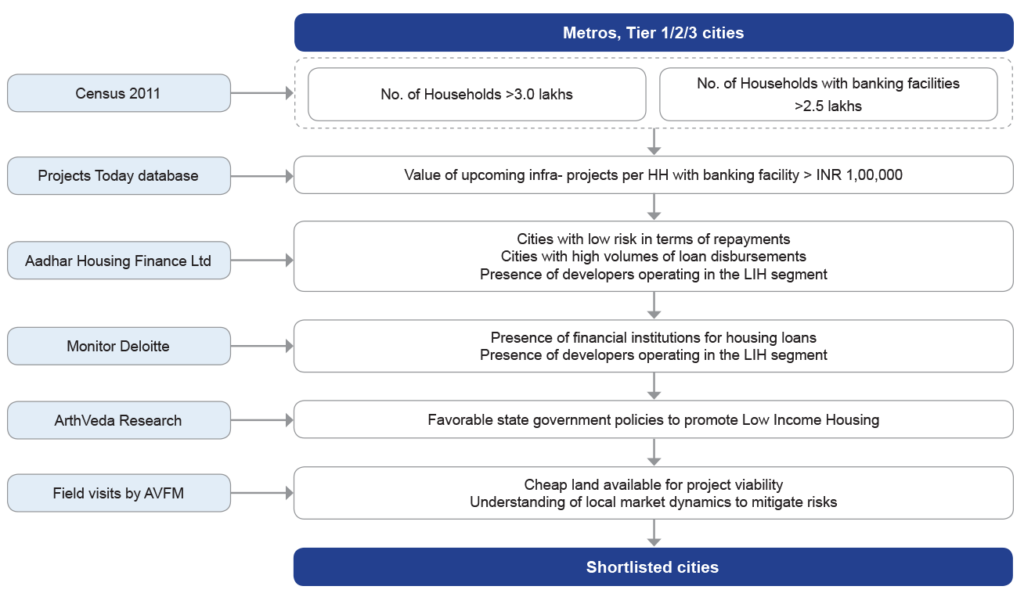

Elimination of unviable markets– While in metros, high-income housing has significantly excess supply, other cities have broadly-balanced demand-supply dynamics in the segment. At the other end of the spectrum, there exists an all- pervasive and materially high demand for low-income housing. We expect this demand to only grow over time due to factors such as general rise in per-capita income, rise in Lower middle- class and increase in number of nuclear families;

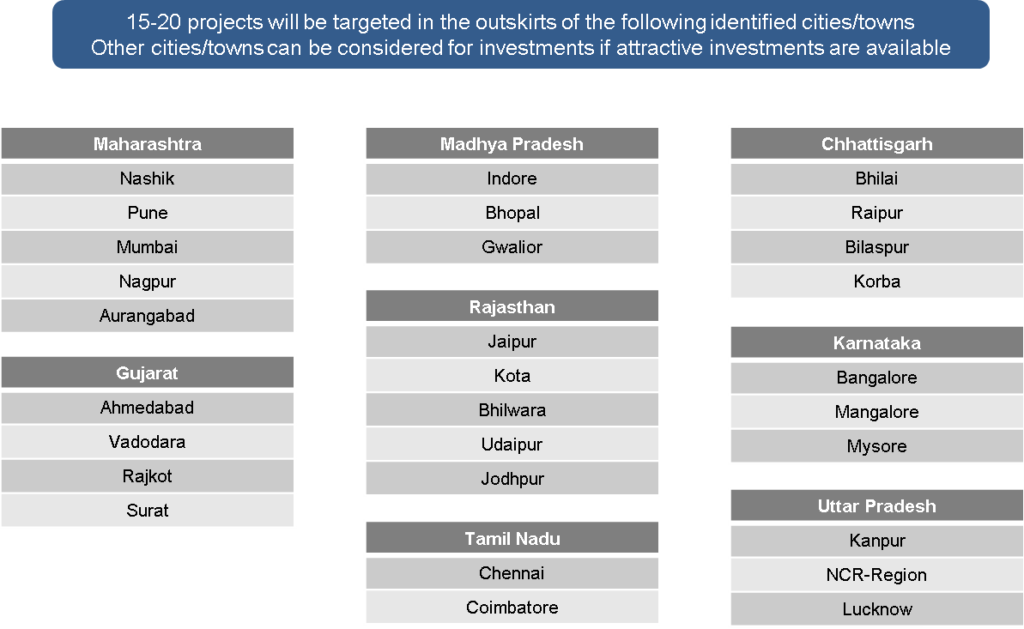

Elimination of unviable cities– As discussed, there exists a huge pent up demand in the Low-income segment all across the country but it is not economically viable to construct such housing in metros. In tier-II/III cities and metro outskirts, however, the land prices and construction costs are conducive to executing such projects profitably. So, we chose to concentrate only on metro outskirts and Tier I/II cities.

Entry valuation risk reduction- We started with a large base of Metro outskirts and non-metro cities to ensure that the land-prices are not prohibitive for a profitable project.

Liquidity risk reduction- Then, we selected cities with a population of at least 8.5 lakhs to ensure sufficient market depth.

Exit risk reduction- Subsequently, we identified cities with high pent up demand due to Literally no supply of housing units in the Low-income profile.

Information asymmetry reduction / Execution risk reduction- Finally, we undertook field surveys of these 30 cities to assess micro-markets in terms of prevailing land price, selling price, construction costs and project duration. We also conducted preliminary developer due-diligence by leveraging Aadhar`s branch network and created an LOI (Letter of Intent) pipeline with the most credible and best developers.

Deal-level risk mitigation

We have a detailed process in place involving thorough technical, legal, commercial and financial due-diligence to evaluate each deal during execution followed by continuous monitoring through the deal-life.

1. Investment destination :Cities selection process

2. Investment process